คำอธิบาย

เราปรับแต่งอัลกอริทึมของเราให้เหมาะสมกับสภาพตลาดเสมอ ซึ่งหมายความว่าคุณก็สามารถทำได้เช่นกัน!

ติดตามสถิติตลาดสดของอัลกอริทึม Hedge Grid มืออาชีพได้ที่นี่: เร็วๆ นี้!

HEDGE GRID STRATEGY PRO เป็นอัลกอริทึมการซื้อขายอัตโนมัติขั้นสูงที่พัฒนาโดย Datarum Algorithmica ไม่ใช่แค่กริดง่ายๆ หรือผู้ติดตามแนวโน้มพื้นฐาน แต่เป็น สถาปัตยกรรมการซื้อขายอัจฉริยะหลายชั้น ที่ออกแบบมาเพื่อปรับตัวเข้ากับพลวัตของตลาดผ่านการผสมผสานที่ซับซ้อนของการจัดการตำแหน่ง การรับรู้ความผันผวน และการควบคุมความเสี่ยงแบบไดนามิก

สำหรับราคาเพิ่มเติม $90 เรามีการสมัครสมาชิกแบบพิเศษ 1 เดือนที่ให้คำแนะนำการติดตั้งแบบตัวต่อตัว คู่มือ PDF การทดสอบย้อนหลัง 5 cbotset เพื่อความสามารถในการทำกำไร และอัปเดตข่าวสารตลาดรายวัน

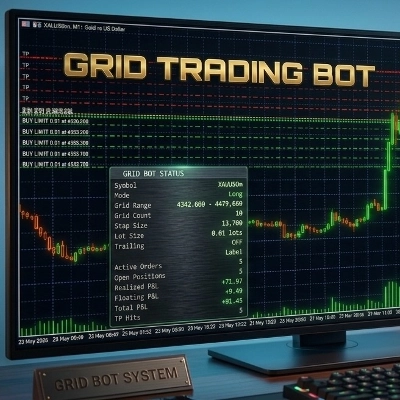

ระบบอัตโนมัติแบบอัลกอริทึมนี้จะยกระดับการซื้อขายของคุณไปอีกขั้น Hedge Grid Strategy Pro เป็นเครื่องมือซื้อขายอัตโนมัติที่มีการปรับใช้กลยุทธ์ได้ ซึ่งผู้ซื้อขายสามารถปรับแต่งได้ด้วยรายการพารามิเตอร์และการตั้งค่าที่ยาวมาก อัลกอริทึม HEDGE GRID STRATEGY PRO ตรวจจับข้อมูลโครงสร้างตลาด สภาพสภาพคล่อง ผสมผสานกับข้อมูลความผันผวนและเงื่อนไขตลาดความผันผวนสูง/ต่ำที่ตั้งค่าไว้ พร้อมกับเงื่อนไข stochastic random walk ที่ขายเกิน/ซื้อมากเกินไป และ +10 ประเภทค่าเฉลี่ยเคลื่อนที่ (Hull, Double, Triple Exponential) ช่วงแนวโน้มและตัวกรอง อัลกอริทึมยังมีฟีเจอร์การทำนายความผันผวนเพื่อระบุสัญญาณการเบรกเอาต์และความผันผวนสูงในเวลาจริง ชุดตัวชี้วัดทั้งหมดนี้ทำงานร่วมกับการจัดการตำแหน่ง ความเสี่ยง ตัวกรองสเปรดและสลิปเพจ โดยผู้ซื้อขายสามารถเลือกเปิดใช้งานฟีเจอร์ hedge-grid ที่รุนแรงขึ้น หรือคงขนาดล็อตแบบคงที่โดยไม่มีตัวคูณ การซื้อขายสามารถส่งผ่าน HEDGE GRID STRATEGY PRO ด้วยฟีเจอร์ FOK และการเข้ารหัส Iceberg มีการตั้งค่าตัวกรองชั่วโมงปกติ จำนวนการซื้อขายสูงสุดต่อวัน เป้าหมายกำไรต่อวันที่เปิดใช้งานได้ สถานะแผงควบคุม และการบันทึกสัญญาณอย่างละเอียด

ระบบทั้งหมดนี้ซับซ้อนยิ่งขึ้นด้วยเครื่องมือเฉพาะ เช่น พารามิเตอร์ความเหมาะสมแบบกำหนดเอง ชั้นคำสั่งซื้อ/ขายในตลาดที่เปิดใช้งานได้ สัญญาณทั้งหมดของอัลกอริทึมไม่ได้ถูกประมวลผลในระบบเกตและตัวกรองแบบคลาสสิกซึ่งเป็นคอขวดทางตรรกะที่ทำให้ความตอบสนองของอัลกอริทึมช้าลง ที่ Datarum Algorithmica เราได้นำวิธีเฉพาะตัวมาแก้ปัญหาการเกตและการกรองเกินด้วยวิธีที่ออกแบบบนแคลคูลัสขั้นสูง

ที่ Datarum Algorithmica เรามุ่งมั่นที่จะนำเสนออัลกอริทึมการซื้อขายคุณภาพสูงที่ไม่ธรรมดา พร้อมใช้งานในตลาดจริง เป้าหมายสำคัญของเราคือการมอบระบบการซื้อขายอัลกอริทึมที่ซับซ้อนให้กับผู้ซื้อขายที่พร้อมเผชิญกับความท้าทายในสภาพตลาดจริง เพื่อเอาชนะตลาด

ใครเหมาะกับสิ่งนี้?

HEDGE GRID STRATEGY PRO ออกแบบมาสำหรับ ผู้ซื้อขายที่มีประสบการณ์และนักลงทุนอัลกอริทึม ที่เข้าใจความซับซ้อนของการซื้อขายแบบกริด การป้องกันความเสี่ยง และการจัดการตำแหน่งแบบไดนามิก ชุดพารามิเตอร์ที่กว้างขวาง (ตัวเลือกที่ปรับแต่งได้ 100 รายการ) มอบความยืดหยุ่นที่ไม่มีใครเทียบได้สำหรับผู้ที่ต้องการปรับแต่งทุกแง่มุมของพฤติกรรมระบบ

ผลิตภัณฑ์นี้ไม่แนะนำสำหรับผู้เริ่มต้น เว้นแต่จะเต็มใจเรียนรู้ ความซับซ้อนของกลยุทธ์ต้องการความเข้าใจที่มั่นคงเกี่ยวกับกลไกการซื้อขาย หลักการจัดการความเสี่ยง และความสามารถในการตีความผลการทดสอบย้อนหลัง อย่างไรก็ตาม Datarum Algorithmica ให้ความช่วยเหลือเต็มที่ แก่ลูกค้าที่ต้องการคำแนะนำในการตั้งค่า การปรับแต่ง และการใช้งานจริง มีการสนับสนุนเพื่อช่วยให้คุณใช้ประโยชน์จากความสามารถของระบบและสอดคล้องกับวัตถุประสงค์การซื้อขายของคุณ

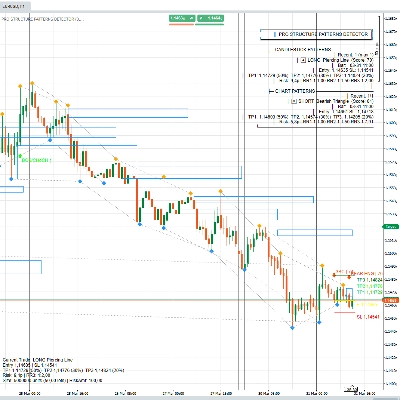

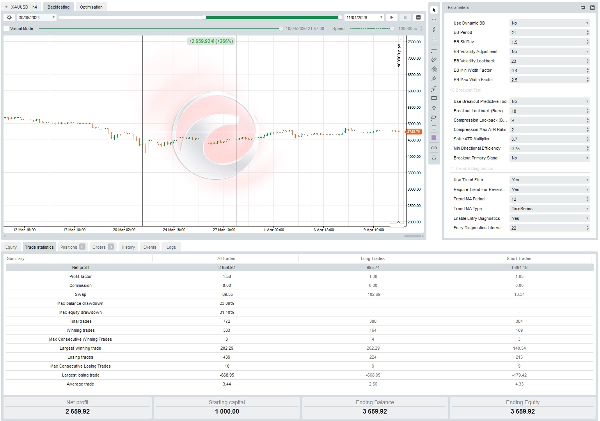

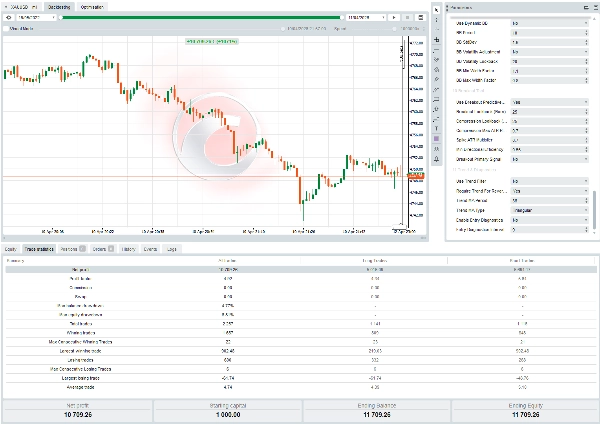

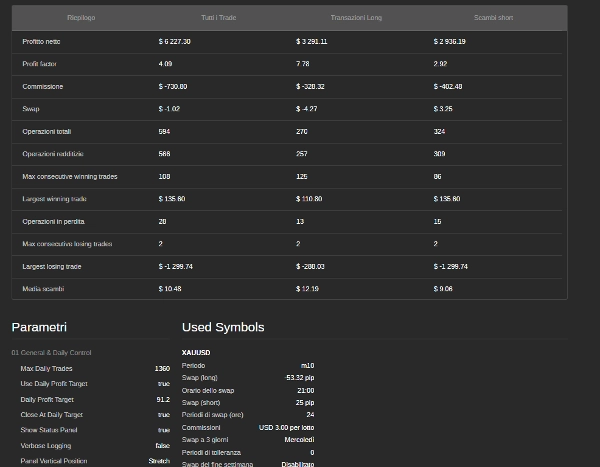

มาตรฐานประสิทธิภาพ — การทดสอบย้อนหลังด้วยข้อมูล Tick

กลยุทธ์ได้รับการตรวจสอบอย่างเข้มงวดโดยใช้ ข้อมูลประวัติ tick-by-tick ซึ่งเป็นรูปแบบการทดสอบย้อนหลังที่เข้มงวดที่สุด ผลลัพธ์ตามรายงานที่แนบมานี้แสดงให้เห็นถึงความแข็งแกร่งของระบบในช่วง ระยะเวลาทดสอบ 2 เดือนและ 20 วัน (18 เมษายน 2026 – 8 กรกฎาคม 2026) บน XAUUSD ด้วย กรอบเวลา m10.

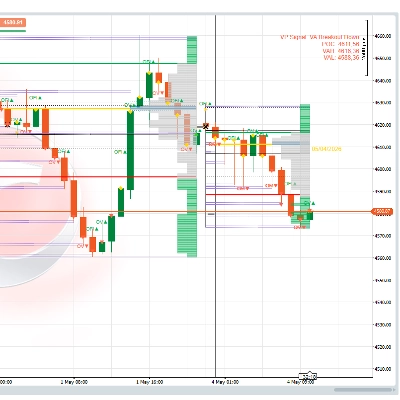

การตรวจสอบแบบ Walk-Forward Live — ความมุ่งมั่นต่อประสิทธิภาพ

Datarum Algorithmica มุ่งมั่นมากกว่าการสัญญาผลลัพธ์จากการทดสอบย้อนหลังเท่านั้น HEDGE GRID STRATEGY กำลังอยู่ในขั้นตอน การตรวจสอบตลาดสดแบบ walk-forward — กระบวนการที่ระบบถูกซื้อขายในสภาพตลาดจริงเพื่อยืนยันว่าผลการทดสอบย้อนหลังแปลงเป็นผลลัพธ์สดจริงได้ นี่คือขั้นตอนสำคัญในวงจรการพัฒนาผลิตภัณฑ์ของเรา เพื่อให้แน่ใจว่ากลยุทธ์ทำงานตามที่คาดหวังก่อนนำเสนอแก่สาธารณะ

ลูกค้าที่ซื้อ cBot นี้จะได้รับประโยชน์จาก การติดตามประสิทธิภาพและการอัปเดตอย่างต่อเนื่อง ขณะที่เราปรับปรุงระบบตามข้อเสนอแนะจากตลาดสด ผลการทดสอบย้อนหลังที่ให้ไว้เป็นเพียงจุดเริ่มต้น; ขั้นตอนการตรวจสอบสดคือที่ที่เราพิสูจน์คุณค่าของกลยุทธ์ในตลาดที่สำคัญจริงๆ

สรุป

HEDGE GRID STRATEGY เป็นระบบซื้อขายอัตโนมัติหลายชั้นที่ซับซ้อนซึ่งผสมผสานการซื้อขายแบบกริดที่ปรับตัวได้ การป้องกันความเสี่ยงแบบไดนามิก การกำหนดขนาดตำแหน่งอย่างชาญฉลาด และเครื่องยนต์รวมการตัดสินใจที่ทรงพลัง สร้างขึ้นสำหรับผู้ซื้อขายที่มีประสบการณ์ซึ่งต้องการประสิทธิภาพและพร้อมที่จะใช้เครื่องมือที่ซับซ้อนแต่มีความสามารถสูง

ด้วยประวัติการทดสอบย้อนหลังที่พิสูจน์แล้ว กระบวนการตรวจสอบสดอย่างต่อเนื่อง และการสนับสนุนเต็มรูปแบบจาก Datarum Algorithmica cBot นี้เป็นโซลูชันการซื้อขายที่จริงจังสำหรับผู้ที่พร้อมยกระดับการซื้อขายอัลกอริทึมของตน

⚠️ ข้อจำกัดความรับผิดชอบที่สำคัญ

- ไม่มีการรับประกันประสิทธิภาพ: การซื้อขายเครื่องมือทางการเงินมีความเสี่ยงสูง ผลการดำเนินงานในอดีต รวมถึงผลการทดสอบย้อนหลังหรือการเล่นซ้ำทางประวัติศาสตร์ ไม่ได้บ่งชี้ถึงผลลัพธ์ในอนาคต ผู้พัฒนาไม่รับประกันความสามารถในการทำกำไร ความสม่ำเสมอ หรือพฤติกรรมการขาดทุนในตลาดสด

- การพึ่งพาตลาดและโบรกเกอร์: ผลลัพธ์จริงแตกต่างกันตามคุณภาพการดำเนินการของโบรกเกอร์ สภาพสเปรด สลิปเพจ สภาพคล่อง ความผันผวนของข่าวสาร และโครงสร้างพื้นฐานเซิร์ฟเวอร์ ตัวกรองและตรรกะการป้องกันความเสี่ยงของอัลกอริทึมสมมติว่ามีสภาพแวดล้อมการดำเนินการที่เสถียรและหน่วงเวลาต่ำ

- ความรับผิดชอบของพารามิเตอร์: การตั้งค่าทั้งหมด (ระยะห่างกริด ตัวคูณ ความเสี่ยงต่อการซื้อขาย ตัวกรองช่วงเวลา ขนาดล็อต ฯลฯ) สามารถปรับได้โดยผู้ใช้ การตั้งค่าที่ไม่เหมาะสมอาจเพิ่มความเสี่ยง ทำให้เกินขีดจำกัดมาร์จิ้น หรือทำให้ตำแหน่งซ้อนกันโดยไม่ตั้งใจ ผู้ใช้ต้องทดสอบชุดพารามิเตอร์อย่างละเอียดในสภาพแวดล้อมจำลองก่อนใช้งานจริง

- ใช้งานด้วยความเสี่ยงของคุณเอง: โดยการติดตั้งหรือใช้งาน CBOTs คุณรับทราบว่าได้อ่าน เข้าใจ และยอมรับข้อกำหนดทางเทคนิค ความรับผิดชอบในการตั้งค่า และการเปิดเผยความเสี่ยงทั้งหมดแล้ว ผู้พัฒนาไม่รับผิดชอบต่อความสูญเสีย การเรียกมาร์จิ้น ข้อผิดพลาดของแพลตฟอร์ม หรือความเบี่ยงเบนในการดำเนินการที่เกิดจากการซื้อขายสด

- เครือข่ายการสื่อสารอิเล็กทรอนิกส์ ECN (การเงิน/การซื้อขาย): ระบบคอมพิวเตอร์ที่จับคู่คำสั่งซื้อและขายสำหรับหลักทรัพย์โดยอัตโนมัติ ช่วยให้โบรกเกอร์รายใหญ่และผู้ซื้อขายรายย่อยซื้อขายโดยตรงโดยไม่ต้องมีคนกลางเช่นผู้เชี่ยวชาญตลาดหลักทรัพย์ คุณภาพของเครื่องจับคู่และการเติมคำสั่งของโบรกเกอร์แตกต่างกันไปในอุตสาหกรรมและต้องการให้ผู้ซื้อขายติดตามสลิปเพจและสเปรดอย่างใกล้ชิด จำกัดสเปรดสูงสุดและสลิปเพจสูงสุดเพื่อให้ได้การจับคู่คำสั่งที่เหมาะสม สำคัญที่ต้องเข้าใจว่าโต๊ะโบรกเกอร์มักไม่จับคู่กลยุทธ์อัลกอริทึมของผู้ซื้อขายรายย่อย เนื่องจากข้อกำหนดทางเทคนิคของ VPS ที่มีความหน่วงต่ำกว่า 1ms และการเลือกเส้นทางของโบรกเกอร์ CFDs เป็นราคาสังเคราะห์ ไม่ได้เคลียร์กลางที่ตลาดหลักทรัพย์ แต่จับคู่โดยอัลกอริทึมที่โต๊ะโบรกเกอร์

ข้อสำคัญเกี่ยวกับข้อกำหนดการปรับแต่ง

อัลกอริทึมนี้ออกแบบมาสำหรับผู้ซื้อขายทั้งมือใหม่และมืออาชีพ แต่ไม่เหมาะสำหรับผู้ซื้อขายที่ขี้เกียจ สำหรับแต่ละเครื่องมือทางการเงินที่คุณต้องการซื้อขาย ไม่ว่าจะเป็นคู่สกุลเงิน ดัชนี สินค้าโภคภัณฑ์เช่นทองหรือเงิน หรือหุ้นรายตัว คุณต้องดำเนินกระบวนการปรับแต่งของคุณเองเพื่อหาการตั้งค่าที่เหมาะสม พฤติกรรมตลาดแตกต่างกันอย่างมากระหว่างเครื่องมือ และสิ่งที่ทำงานได้ดีในสัญลักษณ์หนึ่งอาจไม่ทำงานในอีกสัญลักษณ์หนึ่งหากไม่มีการปรับแต่งที่เหมาะสม อัลกอริทึมนี้มีกรอบงานคุณภาพสูงและเครื่องมือปรับแต่งความเหมาะสมที่เป็นเอกลักษณ์ แต่คุณต้องเต็มใจลงทุนความพยายามเพื่อปรับให้เข้ากับตลาดที่คุณเลือก นี่คือเครื่องมือที่แม่นยำสำหรับผู้ซื้อขายที่จริงจังและกระตือรือร้นซึ่งเข้าใจว่าการปรับตัวเข้ากับตลาดคือกุญแจสู่ความสามารถในการทำกำไรในระยะยาว

ผลการดำเนินงานในอดีต รวมถึงผลการทดสอบย้อนหลังที่นำเสนอสำหรับ XAUUSD ไม่รับประกันผลลัพธ์ในอนาคต ประสิทธิภาพของอัลกอริทึมจะแตกต่างกันตามสภาพตลาด คุณภาพการดำเนินการของโบรกเกอร์ ความหน่วงเวลา และการตั้งค่าพารามิเตอร์ ไม่มีการรับประกันว่า บัญชีใดจะได้กำไรหรือขาดทุนเหมือนกับที่แสดงในผลการทดสอบย้อนหลัง

อัลกอริทึมต้องการการปรับแต่งเฉพาะเครื่องมือ พารามิเตอร์ที่ทำงานได้ดีในสัญลักษณ์หรือกรอบเวลาใดอาจทำให้เกิดการขาดทุนในอีกสัญลักษณ์หนึ่ง ผู้ใช้ต้องรับผิดชอบในการทดสอบและตรวจสอบด้วยตนเองก่อนใช้งานจริง

สงวนลิขสิทธิ์ © Datarum Algorithmica ห้ามทำซ้ำ แจกจ่าย ดัดแปลง แยกวิเคราะห์โค้ด หรือใช้เพื่อสร้างผลงานอนุพันธ์โดยไม่ได้รับอนุญาตเป็นลายลักษณ์อักษรจาก Datarum Algorithmica HEDGE GRID | Advanced Grid & Hedging Algorithm และเทคโนโลยีเฉพาะที่เกี่ยวข้องทั้งหมดเป็นเครื่องหมายการค้าและความลับทางการค้าของ Datarum Algorithmica การใช้งาน ขายต่อ หรือแจกจ่ายโดยไม่ได้รับอนุญาตเป็นสิ่งต้องห้ามอย่างเคร่งครัด

สรุป

Designed for experienced traders and algorithmic investors, the strategy requires instrument-specific optimization and a solid understanding of trading mechanics and risk management. It has been rigorously backtested on tick-by-tick historical data for XAUUSD (m10 timeframe) over a multi-year period and is undergoing walk-forward live validation to confirm real-market performance. The algorithm is ECN-friendly and optimized for low-latency VPS environments.

Risk management tools include stop loss, take profit, trailing stop loss, break-even, session filters, and daily profit targets. The system supports up to 10 simultaneous positions with a recommended minimum balance of $1,000 and a risk per trade of 5%. Ongoing performance monitoring and user support are provided by Datarum Algorithmica. This tool is suitable for high-frequency scalping and breakout trading styles.

รีวิวจากลูกค้า

5 | 0 % | |

4 | 50 % | |

3 | 50 % | |

2 | 0 % | |

1 | 0 % |