Mô tả

PHIÊN BẢN ĐẦY ĐỦ (tần suất cao và các tham số tối ưu hơn) phát triển vào tháng 9 năm 2025

Chiến lược này được thiết kế bởi một sinh viên đại học ngành Công nghệ Tài chính, biến lý thuyết chênh lệch thống kê học thuật thành một bot giao dịch thực tế và có lợi nhuận.

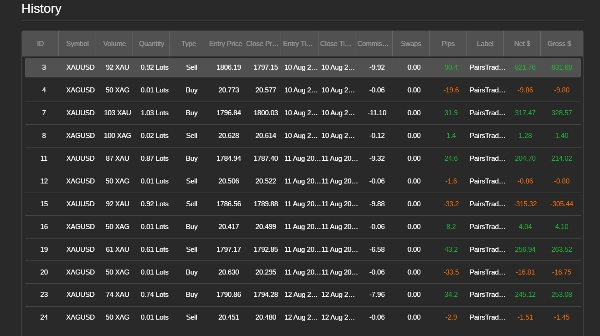

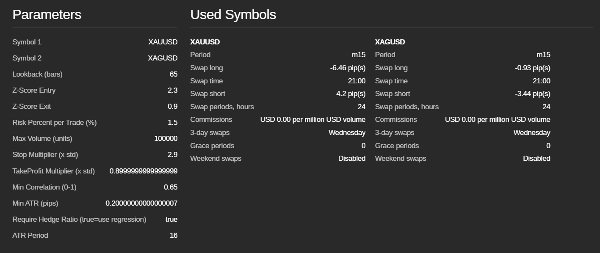

Hệ thống áp dụng giao dịch cặp giữa vàng (XAUUSD) và bạc (XAGUSD), tận dụng mối tương quan mạnh và các mô hình hồi quy về trung bình của chúng.

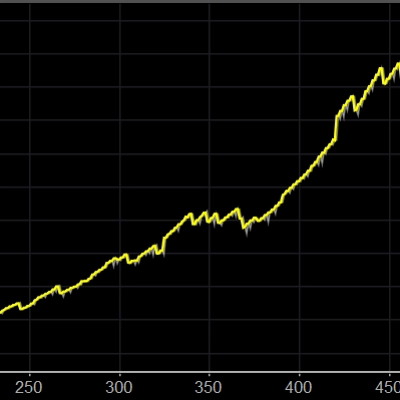

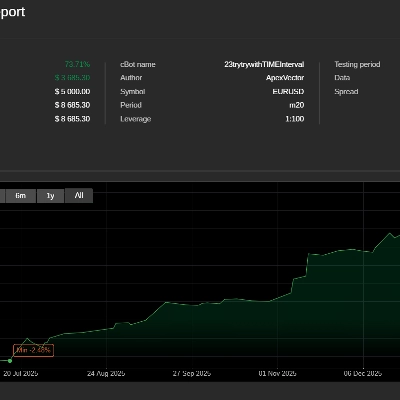

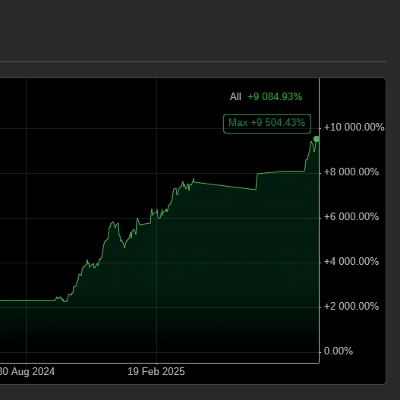

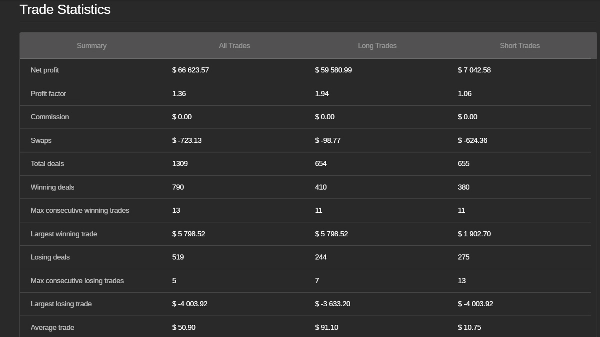

📊 Kết quả kiểm tra lại (vốn ban đầu 5.000 USD và kiểm tra lại trong ba năm gần đây)

- Hiệu suất tổng thể

- Lợi nhuận ròng: $439,768.00

- Hệ số lợi nhuận: 1.3+

- Tổng số giao dịch: 1,298

- Tỷ lệ thắng: 801 (61.7%)

- Số lần thắng liên tiếp tối đa: 13

- Giao dịch trung bình: $338.80

Giao dịch mua dài hạn

- Lợi nhuận ròng: ~$432,725.42

- Hệ số lợi nhuận: 2

- Tổng số giao dịch: 654

- Giao dịch thắng: 410

Giao dịch bán ngắn hạn

- Lợi nhuận ròng: $7,042.58

- Hệ số lợi nhuận: 1.0+

- Tổng số giao dịch: 644

- Giao dịch thắng: 391

⚙️ Các tính năng chính

- Chênh lệch thống kê: Giao dịch phòng ngừa giữa XAUUSD và XAGUSD

- Tín hiệu phân kỳ Z-Score: Phát hiện sự lệch pha của spread so với trạng thái cân bằng

- Dừng lỗ & chốt lời động: Chiến lược thoát điều chỉnh theo biến động

- Bộ lọc Tương quan & ATR: Chỉ giao dịch trong điều kiện mạnh và thanh khoản cao

- Phương pháp trung lập thị trường: Không theo xu hướng, không martingale/lưới

👨🎓 Về tác giả

Được xây dựng bởi một sinh viên đại học Công nghệ Tài chính, bot này là một ứng dụng thực tiễn của các khái niệm tài chính định lượng nâng cao.

Nó đại diện cho cầu nối giữa nghiên cứu học thuật và thực thi thị trường thực tế.

TẤT CẢ CÁC THAM SỐ ĐỀU ĐƯỢC TỐI ƯU.

Tóm tắt

Key features include a market-neutral approach that avoids trend-following, martingale, or grid strategies; dynamic stop-loss and take-profit levels adjusted for volatility; and correlation and Average True Range (ATR) filters to ensure trading only under strong, liquid market conditions. Backtesting over three years with a starting capital of $5,000 demonstrated a net profit of approximately $439,768, a profit factor above 1.3, and a win rate of 61.7% across 1,298 trades. Long trades contributed the majority of profits with a profit factor of 2.0, while short trades showed a profit factor slightly above 1.0.

This bot is optimized for high-frequency trading and is suitable for traders interested in commodity pairs arbitrage strategies focusing on gold and silver markets.

Đánh giá của khách hàng

5 | 33 % | |

4 | 33 % | |

3 | 33 % | |

2 | 0 % | |

1 | 0 % |