GoldAndSilverPairTrading

cBot

버전 1.0, Oct 2025

Windows, Mac, Mobile, Web

4.0

리뷰: 3

13

구매

2

손익비

20%

최대 낙폭

설명

2025년 9월에 개발된 전체 버전(고빈도 및 더 최적화된 매개변수)

이 전략은 금융기술을 공부하는 대학생에 의해 설계되었으며, 학술적인 통계적 차익거래 이론을 실제 수익성 있는 트레이딩 봇으로 변환했습니다.

이 시스템은 금(XAUUSD)과 은(XAGUSD) 간의 페어 트레이딩을 적용하여 두 자산의 강한 상관관계와 평균회귀 패턴을 활용합니다.

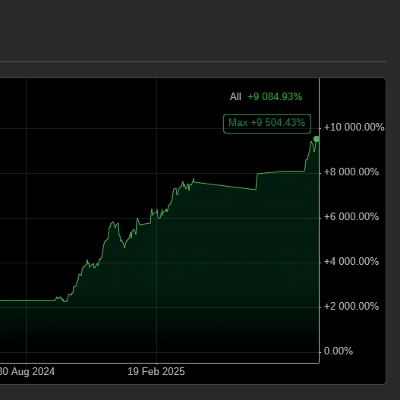

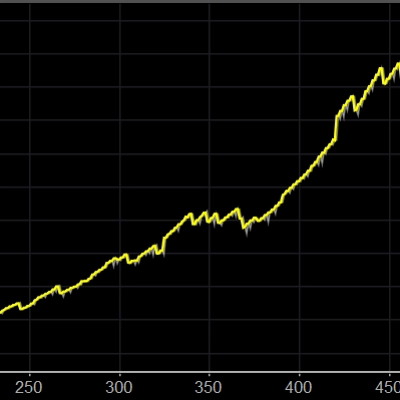

📊 백테스트 결과 (5,000 USD 시작 자본 및 최근 3년간 백테스트)

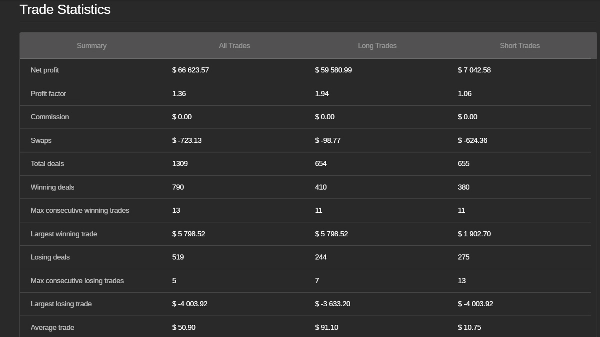

- 전체 성과

- 순이익: $439,768.00

- 수익률 지수: 1.3+

- 총 거래 수: 1,298

- 승률: 801 (61.7%)

- 최대 연속 승리: 13

- 평균 거래 수익: $338.80

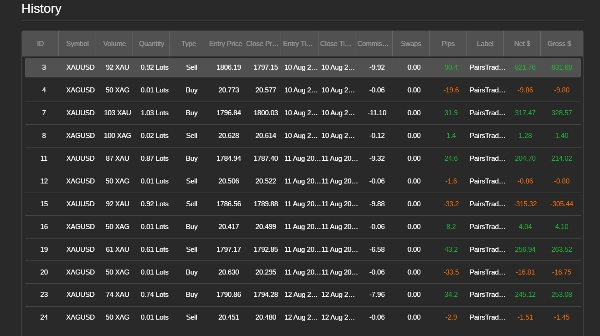

롱 트레이드 (매수)

- 순이익: ~$432,725.42

- 수익률 지수: 2

- 총 거래 수: 654

- 승리 거래 수: 410

숏 트레이드 (매도)

- 순이익: $7,042.58

- 수익률 지수: 1.0+

- 총 거래 수: 644

- 승리 거래 수: 391

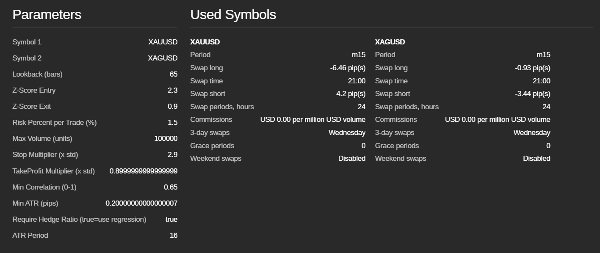

⚙️ 주요 특징

- 통계적 차익거래: XAUUSD와 XAGUSD 간 헤지 거래

- Z-스코어 발산 신호: 균형에서 벗어난 스프레드 감지

- 동적 손절 및 이익 실현: 변동성에 맞춘 종료 전략

- 상관관계 및 ATR 필터: 강하고 유동적인 조건에서만 거래

- 시장 중립적 접근법: 추세 추종 아님, 마틴게일/그리드 아님

👨🎓 저자 소개

금융기술 대학생이 만든 이 봇은 고급 정량 금융 개념의 실용적 구현입니다.

이는 학술 연구와 실시간 시장 실행 간의 다리를 나타냅니다.

모든 매개변수는 최적화되어 있습니다.

요약

AI 요약

GoldAndSilverPairTrading is a statistical arbitrage trading bot designed for pairs trading between gold (XAUUSD) and silver (XAGUSD). Developed by a Financial Technology university student, it applies academic quantitative finance concepts to live market execution. The bot exploits the strong correlation and mean-reversion patterns between these two commodities using Z-score divergence signals to detect spread deviations from equilibrium.

Key features include a market-neutral approach that avoids trend-following, martingale, or grid strategies; dynamic stop-loss and take-profit levels adjusted for volatility; and correlation and Average True Range (ATR) filters to ensure trading only under strong, liquid market conditions. Backtesting over three years with a starting capital of $5,000 demonstrated a net profit of approximately $439,768, a profit factor above 1.3, and a win rate of 61.7% across 1,298 trades. Long trades contributed the majority of profits with a profit factor of 2.0, while short trades showed a profit factor slightly above 1.0.

This bot is optimized for high-frequency trading and is suitable for traders interested in commodity pairs arbitrage strategies focusing on gold and silver markets.

Key features include a market-neutral approach that avoids trend-following, martingale, or grid strategies; dynamic stop-loss and take-profit levels adjusted for volatility; and correlation and Average True Range (ATR) filters to ensure trading only under strong, liquid market conditions. Backtesting over three years with a starting capital of $5,000 demonstrated a net profit of approximately $439,768, a profit factor above 1.3, and a win rate of 61.7% across 1,298 trades. Long trades contributed the majority of profits with a profit factor of 2.0, while short trades showed a profit factor slightly above 1.0.

This bot is optimized for high-frequency trading and is suitable for traders interested in commodity pairs arbitrage strategies focusing on gold and silver markets.

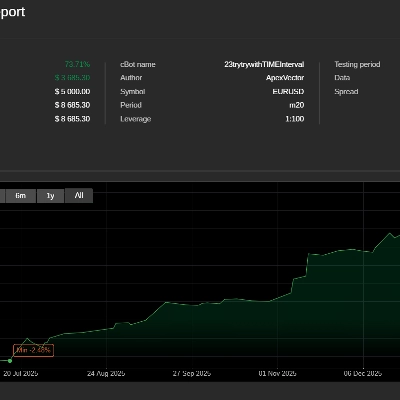

트레이딩 프로필

고객 리뷰

4.0

리뷰: 3

5 | 33 % | |

4 | 33 % | |

3 | 33 % | |

2 | 0 % | |

1 | 0 % |

고객 리뷰

March 9, 2026

The bot implements a genuine statistical arbitrage concept between Gold and Silver using Z-Score divergence and hedge ratio calculations. While the core idea is academically sound, the real backtest results show significant performance degradation. In its current configuration the strategy fails to reproduce the advertised profitability.

October 12, 2025

October 2, 2025

상담

자주 묻는 질문(FAQ)

Commodities

Grid

XAUUSD

Martingale

ATR

트레이딩 봇, 지표, 플러그인 등 cTrader Store에서 제공되는 상품은 제3자 개발자에 의해 제공되며, 이는 단순히 정보 및 기술적 접근을 목적으로 제공된 것입니다. cTrader Store는 중개인이 아니며, 투자 조언, 개인별 추천 또는 향후 성과에 대한 어떠한 보장도 제공하지 않습니다.

이 작성자의 상품 더 보기

가격

10M

거래량

10.64K

핍 수익

23

판매

1.25K

무료 설치