Penerangan

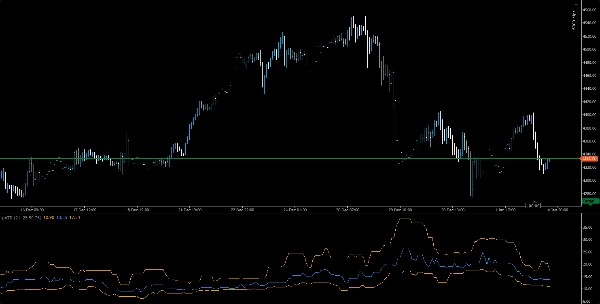

📈 pATR – Purata Julat Benar Peratusan

Ketepatan Volatiliti. Risiko Lebih Bijak. Keunggulan Institusi.

Penunjuk pATR mentakrif semula ATR tradisional dengan menggunakan penapis berasaskan peratusan ke atas nilai julat benar terkini, memberikan pedagang pandangan volatiliti yang berasaskan statistik. Daripada bergantung pada purata mudah, pATR mengira peratusan ke-n intensiti pergerakan harga terkini — membantu anda mengenal pasti zon pecahan, susunan pudar, dan ambang risiko dengan ketepatan pembedahan.

Sama ada anda sedang mengharungi cabaran firma prop atau memperhalusi strategi scalping anda, pATR menyediakan penanda aras volatiliti dinamik yang menyesuaikan diri dengan keadaan pasaran dan mengekalkan risiko anda terkawal.

🔍 Ciri Utama

• ATR Berasaskan Peratusan: Menapis bunyi dan kejadian ekor untuk isyarat volatiliti yang lebih bersih

• Logik Penimbal Bulat: Dioptimumkan untuk kelajuan dan kecekapan memori — tiada kelewatan, tiada kekacauan

• Sedia Mod Cabaran: Sesuai untuk pedagang firma prop yang menguruskan pengurangan modal dan had dagangan

• Visual Bersih: Garis volatiliti oren dengan skala intuitif dan pilihan lapisan

• Serasi Pelbagai Jangka Masa: Gunakan dari M1 hingga H1 untuk pecahan, pudar, atau susunan tren

🧠 Kes Penggunaan

• Pengesahan Pecahan: Gunakan lonjakan pATR untuk mengesahkan kemasukan momentum

• Kalibrasi Risiko: Selaraskan stop-loss dan saiz posisi dengan volatiliti peratusan

• Ujian Semula Strategi:Sahkan susunan dengan ambang volatiliti yang konsisten

🎯 Siapa Yang Sesuai

• Pedagang firma prop yang mencari kawalan risiko berasaskan peraturan

• Scalper dan ahli strategi intraday yang memerlukan penapis volatiliti adaptif

• Pedagang kuantitatif yang mengintegrasikan logik peratusan ke dalam sistem tersuai

• Pendidik dan mentor yang mengajar pelaksanaan berasaskan kesedaran volatiliti

Ringkasan

Key features include an orange volatility line with intuitive scaling and overlay options, compatibility across multiple timeframes from 1-minute to 1-hour charts, and suitability for prop firm traders managing drawdowns and trade limits. pATR helps traders identify breakout zones, fade setups, and risk thresholds with precision.

Use cases cover breakout confirmation through volatility spikes, risk calibration by aligning stop-loss and position sizing with percentile volatility, and strategy backtesting using consistent volatility benchmarks. The indicator is designed for prop firm traders, scalpers, intraday strategists, quantitative traders integrating percentile logic, and educators focusing on volatility-aware execution.

Supported markets include Forex, stocks, indices, commodities, and cryptocurrencies, making pATR a versatile tool for various trading environments.