Description

Amplitude Momentum Label — Adaptive Trend Detection Powered by Volatility

The Amplitude Momentum Labeler unifies multiple advanced concepts:

- Regime Detection — Identifies true trend phases

- Volatility Adaptation — Self-tunes to current market conditions

- Dynamic VWAP — Highlights meaningful pullback and continuation levels

- Roll Spread Estimator — Signals optimal re-entry points during trends

- OPTIMIZATION MODULE — with Self-Optimization Feature**

This creates an intelligent, self-adjusting indicator that delivers clarity, adaptability, and actionable trade zones—without constant manual tweaking.

What Is It?

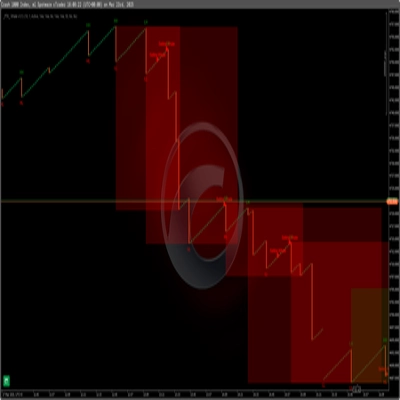

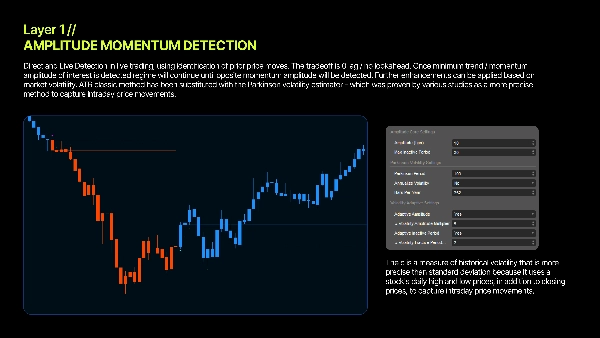

The Amplitude Momentum Labeler is a regime-detection indicator that pinpoints when the market enters or exits upward or downward momentum phases—in real time.

Unlike traditional moving-average crossovers, it measures actual momentum shifts by evaluating price displacement and reversal strength.

The Core Question

Is the market currently in a momentum phase—and in which direction?

To answer this, the indicator tracks:

- Amplitude — how far price has moved;

- Sequence — the order in which highs and lows occur.

A strong move followed by a meaningful reversal marks the beginning of a new momentum regime.

How it Works

1. Measure the Swing

The indicator constantly updates the highest and lowest price extremes.

Their difference—amplitude—defines the market’s current swing size.

2. Detect Reversal

- A sharp decline followed by a strong rally → **Upward momentum**

- A sharp rise followed by a strong decline → **Downward momentum**

3. Confirm Significance

Only reversals exceeding a volatility-adjusted threshold trigger a valid signal.

4. Detect Exhaustion

If price stops progressing, the indicator identifies momentum exhaustion and returns to neutral.

Parkinson Volatility — Adaptive Thresholds

Most indicators use fixed parameters. This one adapts automatically. By using Parkinson Volatility—which incorporates intraday high/low ranges—the indicator adjusts sensitivity based on real market conditions. The result: consistent performance across quiet and volatile environments. ( Statistically proven more efficient than ATR Method )

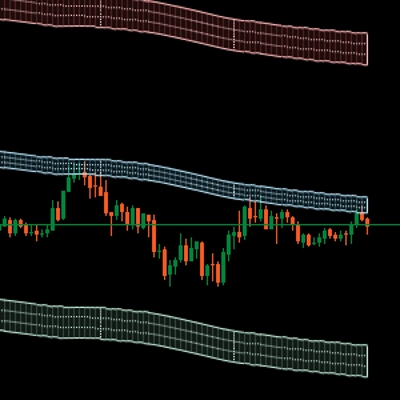

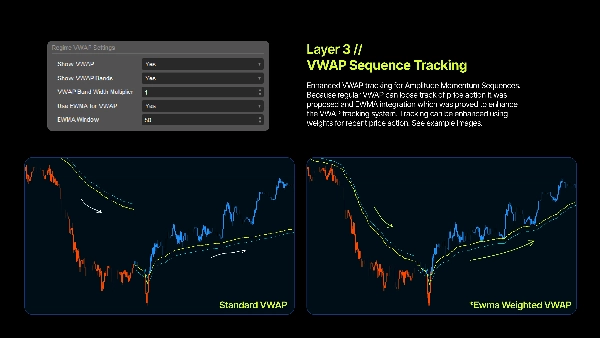

Regime VWAP — Dynamic Levels for Re-Entry

Once a regime is active, the indicator computes a VWAP specific to that trend, providing Dynamic Support and Dynamic Resistance Levels. Institutions rely heavily on VWAP, and price often reacts around it—making it ideal for pullback entries.

EWMA Mode

Enable EWMA to weight recent prices more heavily, creating a smoother, more responsive VWAP curve. Excellent for identifying re-entries during extended trends.

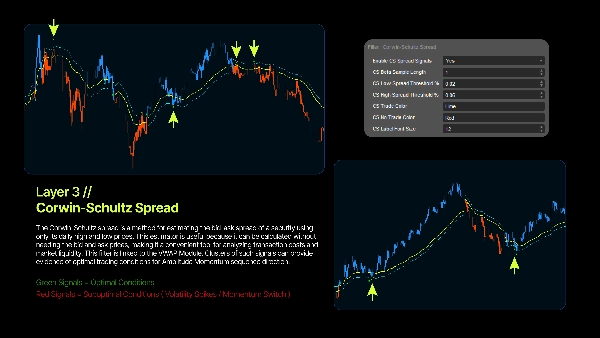

Roll Spread Estimator - Dynamic Filter for Re-Entry

A roll spread estimator is a method for estimating the bid-ask spread from observed trade prices, typically using the serial covariance of price changes. Developed by Roll, it assumes that successive trades alternate between the bid and ask prices, and new information is not constantly moving the "true" price. While simple and foundational, the original method has been refined to address issues like downward bias and poor performance in certain datasets. The estimator is based on the idea that if no new information is released, prices will simply bounce between the bid and ask. It assumes an equal probability of a buy-initiated and a sell-initiated trade.

Usage Benefits

1. Objective Trend Identification - No trendlines. No guesswork. The math defines the regime.

2. Volatility Adaptive - Automatically adjusts to changing conditions using Parkinson Volatility.

3. Clear Entry Zones - Regime VWAP levels help pinpoint intuitive pullback and add-on areas.

4. Defined Regime Boundaries - Know exactly when momentum begins and when it ends.

5. Multi-Timeframe Compatibility - Basis-point normalization ensures consistent behavior on any chart.

The Quantitative Foundation

Logarithmic Returns

Using log returns ensures symmetry, making momentum measurement mathematically robust.

Basis Points

All calculations use standardized bps units (1 bps = 0. 01%), allowing cross-asset consistency.

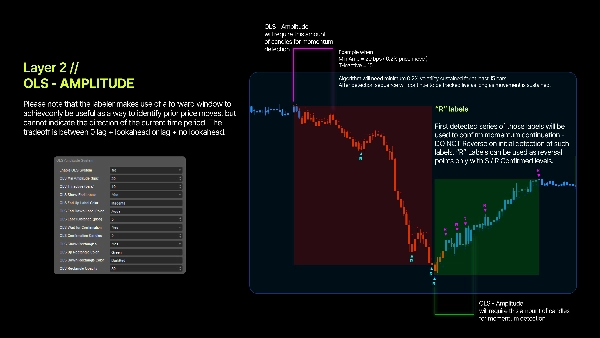

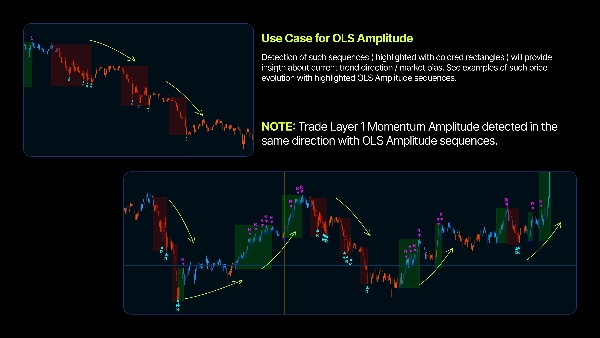

Retracement Detection

Momentum shifts are identified through strong directional moves followed by meaningful counter-moves (V-shaped reversals).

Synthetic Volume

Range and body-based synthetic volume ensures VWAP accuracy for any symbol.

⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽⎽

This tool is for educational and informational purposes only. It is not investment advice. Trading involves risk, and losses can exceed deposits. Past performance does not guarantee future results. You are solely responsible for all trading decisions. The creator is not liable for any financial losses arising from the indicator’s use. Always perform your own analysis before trading.

Summary

Key features include:

- **Regime Detection:** Pinpoints market entry and exit points for momentum trends.

- **Volatility Adaptation:** Uses Parkinson Volatility to self-tune sensitivity based on current market conditions, ensuring consistent performance across varying volatility.

- **Dynamic VWAP:** Calculates a volume-weighted average price specific to each trend regime, providing dynamic support and resistance levels for pullback and continuation entries.

- **Roll Spread Estimator:** Estimates bid-ask spreads to signal optimal re-entry points during trends.

- **Self-Optimization Module:** Automatically adjusts parameters without manual intervention.

The indicator operates by continuously tracking price extremes to measure swing amplitude, detecting significant reversals that exceed volatility-adjusted thresholds, and identifying momentum exhaustion when price progression stalls. It uses logarithmic returns and basis-point normalization for mathematically robust, cross-asset consistency. Synthetic volume calculations enhance VWAP accuracy across symbols.

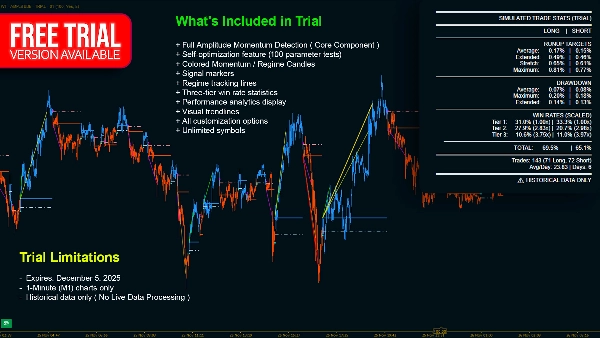

This tool supports multiple markets including Forex, stocks, indices, commodities, and cryptocurrencies, and is compatible with various timeframes. It outputs visual signals and filters to assist traders in objective trend identification and clear entry zone determination.

Customer reviews

5 | 75 % | |

4 | 25 % | |

3 | 0 % | |

2 | 0 % | |

1 | 0 % |

!["Smart Money Concepts (SMC) [Iridio Capital]" logo](https://cdn.ctrader.com/image/webp/28b69fd1-ef54-4bed-9487-07e78e883be4_40934)