Description

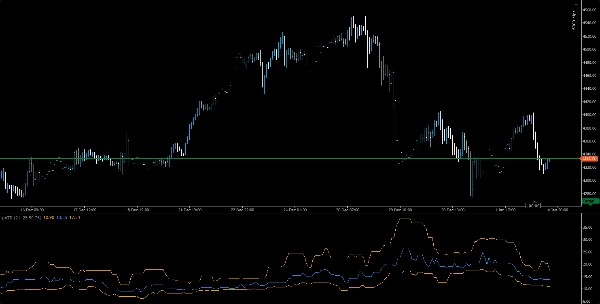

📈 pATR – Percentile Average True Range

Precision Volatility. Smarter Risk. Institutional Edge.

The pATR indicator redefines traditional ATR by applying a percentile-based filter to recent true range values, giving traders a statistically grounded view of volatility. Instead of relying on simple averages, pATR calculates the nth percentile of recent price movement intensity — helping you identify breakout zones, fade setups, and risk thresholds with surgical accuracy.

Whether you're navigating prop firm challenges or refining your scalping strategy, pATR delivers a dynamic volatility benchmark that adapts to market conditions and keeps your risk calibrated.

🔍 Key Features

• Percentile-Based ATR: Filters out noise and tail events for cleaner volatility signals

• Circular Buffer Logic: Optimized for speed and memory efficiency — no lag, no clutter

• Challenge Mode Ready: Ideal for prop firm traders managing drawdown and trade limits

• Clean Visuals: Orange volatility line with intuitive scaling and overlay options

• Multi-Timeframe Compatible: Use across M1 to H1 for breakout, fade, or trend setups

🧠 Use Cases

• Breakout Confirmation: Use pATR spikes to validate momentum entries

• Risk Calibration: Align stop-loss and position sizing with percentile volatility

• Strategy Backtesting: Validate setups with consistent volatility thresholds

🎯 Who It's For

• Prop firm traders seeking rule-based risk control

• Scalpers and intraday strategists needing adaptive volatility filters

• Quantitative traders integrating percentile logic into custom systems

• Educators and mentors teaching volatility-aware execution

Summary

Key features include an orange volatility line with intuitive scaling and overlay options, compatibility across multiple timeframes from 1-minute to 1-hour charts, and suitability for prop firm traders managing drawdowns and trade limits. pATR helps traders identify breakout zones, fade setups, and risk thresholds with precision.

Use cases cover breakout confirmation through volatility spikes, risk calibration by aligning stop-loss and position sizing with percentile volatility, and strategy backtesting using consistent volatility benchmarks. The indicator is designed for prop firm traders, scalpers, intraday strategists, quantitative traders integrating percentile logic, and educators focusing on volatility-aware execution.

Supported markets include Forex, stocks, indices, commodities, and cryptocurrencies, making pATR a versatile tool for various trading environments.